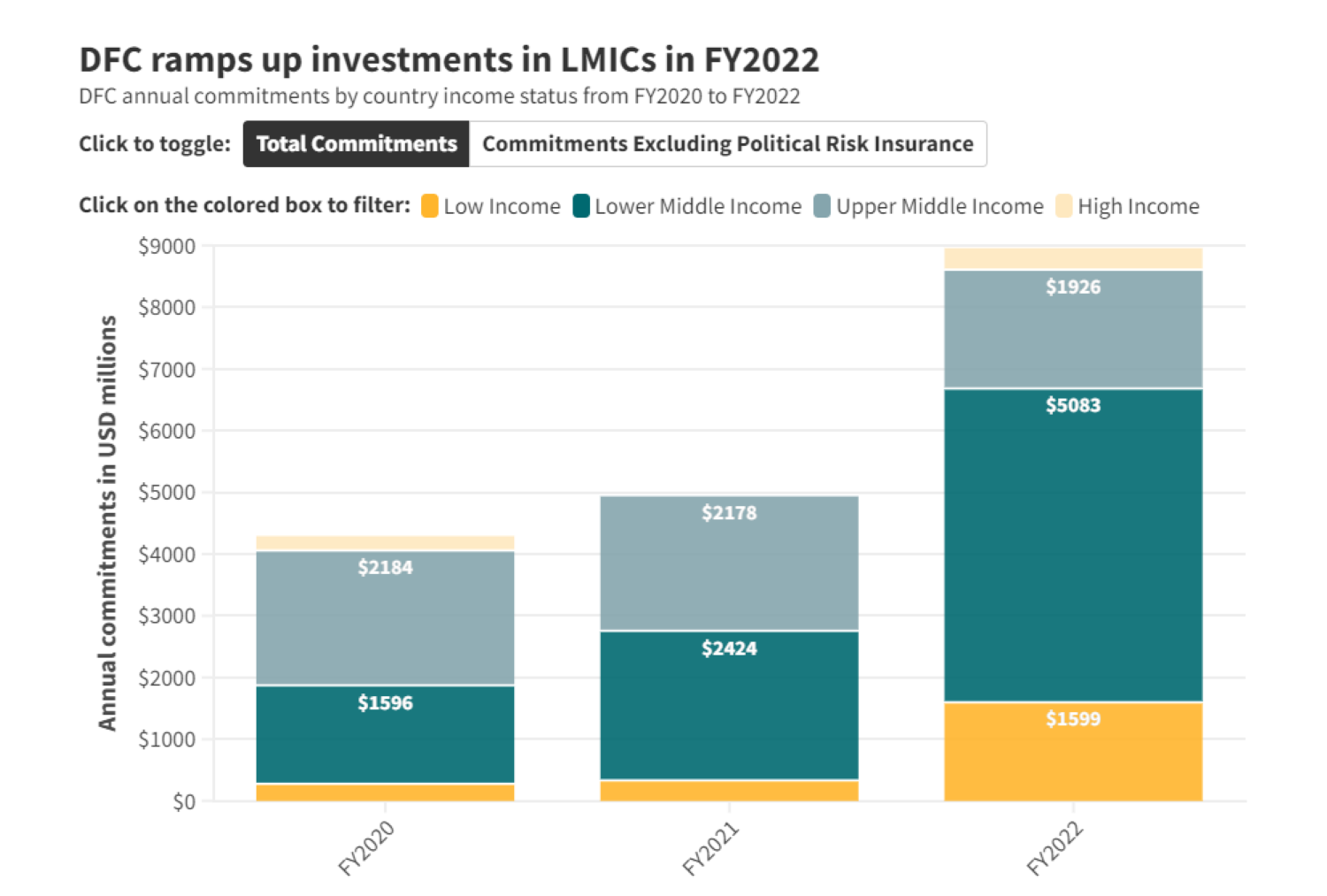

The House of Representatives is scheduled to vote on the Electrify Africa Act later tonight. This legislation would increase the US government’s efforts to promote reliable and affordable electricity for the roughly 600 million Africans that currently live without it. It aims to mobilize all US development tools, ranging from technical assistance grants to risk insurance to long-term debt financing for private investors. Thanks to the Overseas Private Investment Corporation (OPIC), the CBO scored it as budget positive. Electrify Africa has received wide bipartisan support, with over 117 co-sponsors as of last week. Advocacy organizations, like the ONE Campaign (who has roughly 2 million US members), have also been championing this legislation.

Yet, with all major policy initiatives, there are a few dissenting voices. The Club for Growth and Heritage Foundation have been on a crusade to shut OPIC down for years. Since the Electrify Africa Act includes a three-year OPIC re-authorization, then naturally the bill should be killed too. The argument is pretty straightforward. Although, it also lacks an appreciation for US development and foreign policy priorities as well as an understanding of how global capital functions (or doesn’t) in frontier economies. In essence, these groups contend that the U.S. government shouldn’t provide loans, guarantees, or insurance in risky environments where private-sector alternatives are not available. Doing so represents corporate welfare and puts US taxpayers at risk.

Here are quick responses to each of the two arguments:

Corporate Welfare: U.S. investors pay risk-based fees for insurance policies. They also pay risk-adjusted interest rates on OPIC loans. So, where exactly is the corporate handout? Is it because they’re gaining access to longer loan maturities (which are required for many sectors, like power generation in Africa) that U.S. banks aren’t willing to provide? If so, then that isn’t corporate welfare. Instead, OPIC is helping to create market liquidity where it currently doesn’t exist. Once appropriate private financing alternatives become available, then OPIC naturally should step back. This is why OPIC’s Board considers the ‘additionality’ of every proposed transaction before approving it.

Taxpayer Risk: Through portfolio diversification (regions, countries, and sectors), sound due diligence procedures, and risk-adjusted pricing terms, OPIC has operated in the black for 36 consecutive years. However, it purposefully doesn’t seek to maximize profits, nor should it as a US development agency. Instead, OPIC is guided by a double bottom line philosophy – only supporting developmental investments that are also commercially viable.

OPIC antagonists may argue that one logical way of addressing both of these concerns is to charge higher loan and insurance rates. That’d stick it to the US fat-cat investors who are interested in both ‘doing good’ abroad and ‘doing well’. It’d also increase OPIC’s revenues, which would offset any theoretical portfolio meltdown scenarios.

Another alternative is to shut OPIC down and ensure that the US government only promotes its development and foreign policy objectives through grant programs. In this scenario, there would be explicit firewalls between investors and US government agencies. They shouldn’t speak to each other and definitely shouldn’t partner together.

Both of these are overly simplistic propositions. America’s greatest strength is found in the depth of its entrepreneurial class, innovation, and capital base. The US private sector, including investors, should absolutely play a key role in promoting development objectives throughout the world. Businesses and investors often will play that role without any involvement from OPIC or other government agencies. But sometimes, there will be a strong case for OPIC to help unlock private capital for important objectives in places that lack ready access to alternative sources of capital. Such as providing people with reliable power for the first time in Togo, providing healthcare and medical education in Pakistan, or addressing affordable housing shortages in Iraq.

CGD blog posts reflect the views of the authors, drawing on prior research and experience in their areas of expertise.

CGD is a nonpartisan, independent organization and does not take institutional positions.