Recommended

Blog Post

Signed into law in October 2018, the Better Utilization of Investments Leading to Development (BUILD) Act established the new US International Development Finance Corporation (DFC)—bestowing the agency with new tools, a $60 billion portfolio cap, and a seven-year authorization. Even with time still on the clock, lawmakers on Capitol Hill are now beginning reauthorization conversations. The early start seems prudent since advancing consequential legislation—even the bipartisan kind—can take time. And since the development finance institution requires authorization to enter new deals and engages in financing arrangements that span years, the certainty that comes with multi-year reauthorization is vital. But the reauthorization process is also an opportunity to set guidance around DFC’s overall trajectory and give the agency the necessary tools to succeed. This should include a reaffirmation of DFC’s primary objective of advancing development in countries that struggle to access private finance and address issues that have hindered the agency’s ability to fulfill the promise of its authorizing statute.

DFC to date

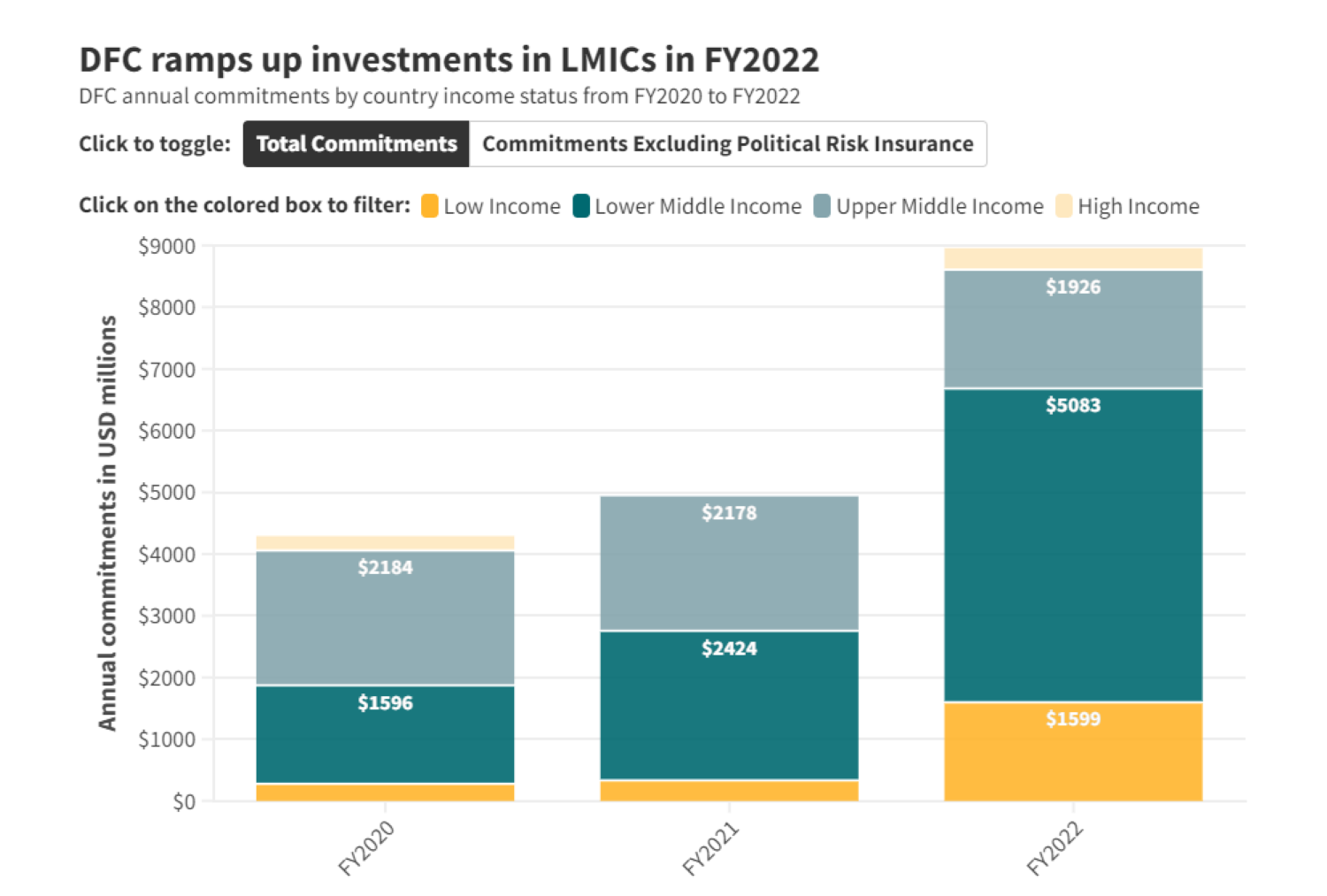

Since its inception, DFC has demonstrated its capacity to rapidly increase its investment volume, making use of a higher portfolio cap. Its annual commitments have doubled over the past four years. But the agency has been subject to criticism (including from some at CGD) for insufficiently prioritizing the poorest countries and the development impact of investments. The reauthorization discussion offers the opportunity for Congress, the administration, and stakeholders to agree on clear guidance and guidelines that will help the agency pursue the right balance among its multiple objectives: boosting the volume of its financing, increasing its mobilization of private finance, maximizing development impact, prioritizing the poorest, and promoting strategic US interests in the developing world.

Having opened its doors in late 2019, DFC, as the new kid on the block, has attracted considerable attention from stakeholders with differing views on what its priorities should be. Some of this has come in the form of pressure to deploy its tools in higher-income countries where the United States has strategic interests, including supporting European allies amid Russia’s war in Ukraine. DFC has expanded its portfolio in Asia and Africa. Still, in FY2023, investments in Europe comprised the largest share of DFC’s annual commitments, with projects focused on supporting Ukraine (a lower-middle-income country) and bolstering energy security in Eastern Europe. While such strategic investments have merit, a tilt too far in that direction risks crowding out DFC’s focus and impact on poverty reduction.

This is not to say the agency has missed its mark on development. DFC has built up a sturdy portfolio in lower-middle-income countries, while piloting innovative approaches to tackle global challenges—for instance, supporting debt-to-nature swaps and the COVAX Rapid Financing Facility. But the BUILD Act reauthorization is an opportunity to recenter DFC’s agenda squarely on development and ensure the agency is maximizing impact and crowding in the private sector while defining clearly when operations in UMICs are warranted to promote US economic policy interests, spillover gains for LICs and LMICs, and investment in global public goods (GPGs). Here are a few ways we think that can be done.

Priorities for DFC reauthorization

1. Give DFC enough runway. The BUILD Act had an ambitious vision for the new US development finance institution, providing DFC with more than double the headroom of OPIC. Though it took more than a year for DFC to open its doors after BUILD’s passage, the agency has been growing ever since—adding staff and expanding its portfolio. Given recent momentum and the importance of lead time for establishing a project pipeline and getting deals off the ground, Congress should look to double DFC’s portfolio cap, known as its maximum contingent liability, from $60 billion to $120 billion, and reauthorize the agency for another seven years. While a doubled portfolio cap appears ambitious, $120 billion still represents less than half a percent of the current GDP of emerging market and developing economies (EMDEs)[1] and will help ensure DFC has sufficient headroom.

2. Tie up three budget fixes:

-

Equity fix. The BUILD Act provided DFC with the authority to make direct equity investments. This was viewed as an important innovation since OPIC was sometimes kept out of deals because it lacked this authority. Unfortunately, the illogical budget treatment of DFC’s equity investments has curbed the agency’s ability to make the best use of this instrument. Reauthorization provides an opportunity for Congress to ensure DFC’s equity deals are treated as the long-term investments that they are rather than scoring them as a grant which treats them as immediate and total losses (i.e. assumes that DFC never recuperates the investment or makes a return).

-

Political Risk Insurance (PRI) fix. DFC has also encountered an obstacle in the budget treatment of its political risk insurance tool. This is not a new tool for DFC and was commonly employed by OPIC. In the upcoming reauthorization, Congress should emphasize that PRI should be treated and scored as a contingent liability—appropriately reflecting the risk of claims and payout, similar to how it was treated under OPIC.

-

Fee fix: Like OPIC, DFC can charge borrowers modest fees. But unlike its predecessor, which could use fees to cover certain project-specific transaction costs, DFC must account for these fees in its administrative budget capped by congressional appropriators. The administration’s FY2024 budget request and the draft Senate State and Foreign Operations appropriations bill signaled appetite to make the fix, but reauthorization offers an opportunity to codify a permanent solution and give DFC this modest (but important) flexibility afforded to its predecessor, OPIC.

3. Just say no to high-income countries. The BUILD Act made no explicit reference to high-income countries (HICs), directing DFC to prioritize LIC and LMIC investments while allowing for UMIC investments that met specified criteria. In December 2019, a last-minute addition to an end-of-year spending package authorized the agency to pursue energy deals in UMICs and HICs in Europe, without the need to justify the investment on development grounds.[2] The provision was born out of growing (valid) concerns about Russia—but created a major loophole enabling inefficient investments. From FY2020 through FY2023, around 4.5 percent of DFC’s commitments (in dollar terms) have been in HICs. [3] We do not see a development rationale for providing financing to the private sector in countries that enjoy low-cost access to external capital markets and may even have deep domestic capital markets. For this reason, we think the reauthorization should definitively close the door on HIC financing.

4. Stronger standards and guidelines for operating in upper-middle-income countries. Under the BUILD Act, DFC support in UMICs must be certified as furthering US economic and foreign policy interests and is designed to deliver “significant development outcomes” or provide development benefits to the poorest in that country. In practice, the authority to make this determination has been delegated to the State Department. The certification process is cumbersome and time-consuming. We propose that DFC’s Board make the determination instead. DFC’s Board, with representation across the relevant agencies—including State, USAID, Treasury, and Commerce—has the range of perspectives and expertise needed to make well-founded determinations. To further strengthen the decision-making process, ensure compliance with the intent of the criteria in the Build Act, and increase transparency, we recommend the addition of criteria that would guide the Board and ensure transactions in UMICs contribute to well-defined objectives. Reauthorization legislation should direct DFC to share with the Board how its proposed UMIC project would fulfill the following two requirements:

(1) Private investors would not finance the project without DFC’s participation.

(2)The project meets at least one of the criteria specified in the table below (Table 1. Criteria for DFC Transactions in UMICs). The criteria define specific and significant benefits from the transaction for: (1) the United States and its allies, (2) LICs and LMICs, and/or (3) global public goods.

|

Table 1. Criteria for DFC Transactions in UMICs |

||

|---|---|---|

|

Category 1: Gains for the US and its allies |

||

|

1.1 |

The transaction builds supply chains for essential goods and services (e.g., vaccines and therapeutics) or material inputs promoting US economic, climate, and security interests (e.g., rare earth minerals). |

|

|

1.2 |

The transaction strengthens UMIC labor and business practices in ways that meet US standards and promotes transformational improvements in gender equity outcomes. |

|

|

1.3 |

The transaction supports a UMIC affected by conflict or a catastrophic natural disaster. |

|

|

1.4 |

The transaction supports a UMIC disproportionately impacted by refugee crises. |

|

|

Category 2: Gains for LICs and LMICs |

||

|

2.1 |

The transaction promotes the spread of poverty-reducing innovations in technology or business models from UMICs to LICs and LMICs. |

|

|

2.2 |

The transaction strengthens regional integration that includes and benefits LICs and LMICs. |

|

|

2.3 |

The transaction supports UMIC exports of goods and services that benefit LIC and LMIC energy transitions or food security. |

|

|

2.4 |

The transaction builds low-carbon regional transport and energy networks. |

|

|

Category 3: Gains for GPGs |

||

|

3.1 |

The transaction has significant positive spillovers for combatting global climate change and its costs. |

|

|

3.2 |

The transaction preserves or expands natural capital and/or biodiversity. |

|

|

3.3 |

The transaction reduces vulnerability and resilience to—and recovery from—global pandemics. |

|

5. Boost private finance mobilization. Mobilizing private financing should be core to DFC’s mission. DFC should use taxpayer funds as efficiently as possible to catalyze larger amounts of private finance for development. Congress should use reauthorization as an opportunity to reinforce this point and encourage DFC to report annually on private capital mobilization and set targets for its future investments. It would be appropriate for DFC to set a high bar for mobilization of private finance in UMICs (say each dollar DFC investment should mobilize at least two dollars in private finance) and a more modest target for low-income countries and lower-middle-income countries. This would encourage DFC to be more catalytic in more advanced economies where capital markets are deeper and private financing is more abundant and affordable.

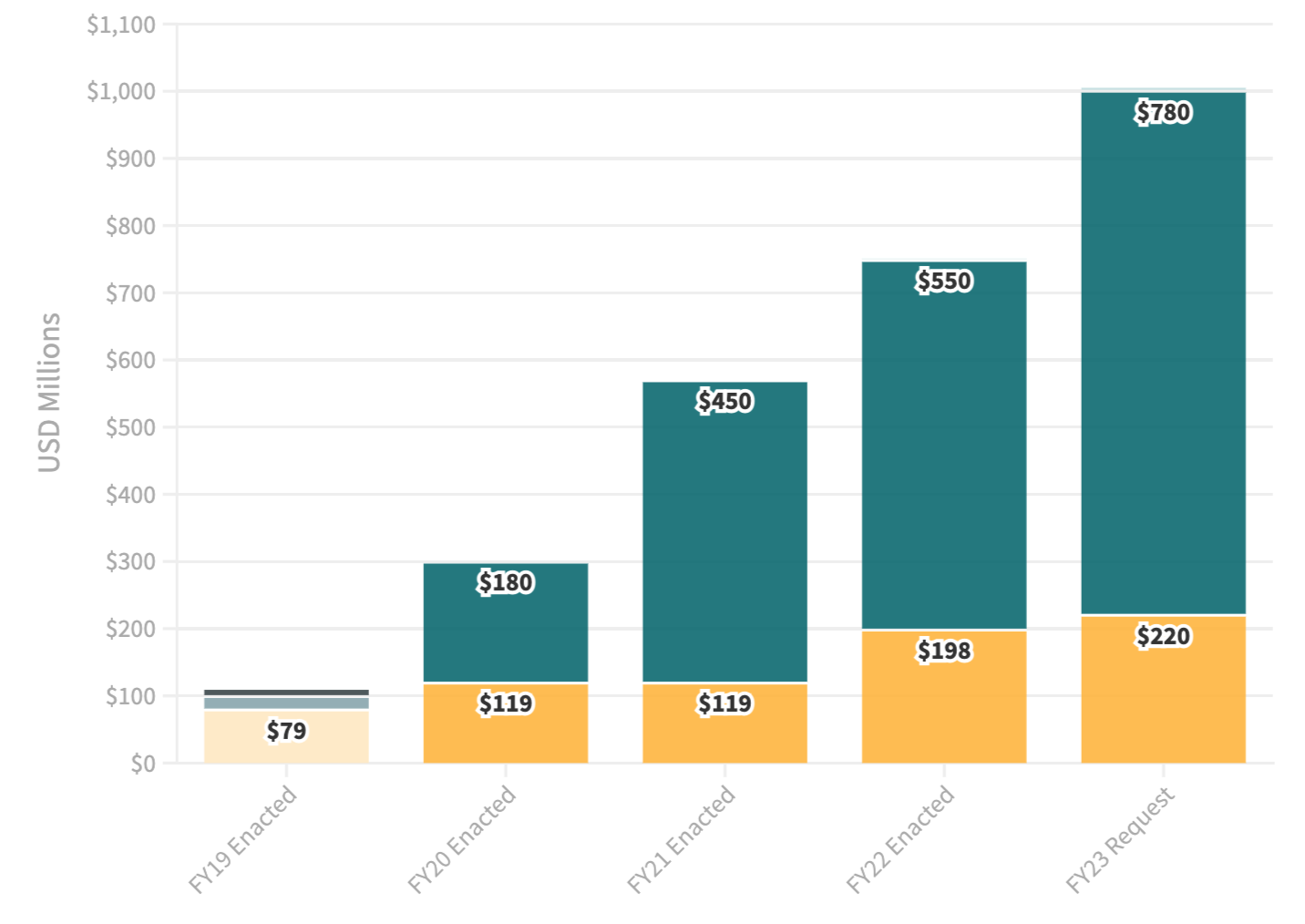

6. House the sovereign loan guarantee (SLG) program. The US sovereign loan guarantee program is among the US government’s most cost-effective and under-utilized instruments. While the BUILD Act authorized the transfer of the program to DFC or another federal agency, it didn’t mandate that move. The USAID staff who administered the program before the passage of the BUILD Act were transferred to DFC with USAID’s Development Credit Authority. But, at the time, the program still had substantial remaining exposure that—if transferred to DFC—would have accounted for a large share of the new agency’s increased headroom. With few good options on the table, the program has been in limbo over the past five years. Historically, the sovereign loan guarantee has been deployed as a foreign policy tool, but our colleagues published a proposal last year to revive and revamp the program with a development focus. Consistent with their vision, we see an opportunity for DFC to play the fiduciary role for the program. The reauthorization legislation should revisit the sovereign loan guarantee program, formalizing a policy framework and establishing cross-agency governance of the program.

7. Transparency first (including on development impact). As the official US development finance institution, DFC has an important responsibility and is required by the BUILD Act to publish timely, detailed, accessible information about its portfolio. While DFC has made improvements in making its project data readily available, stakeholders still face significant barriers in using and understanding the data. Further, Congress should direct DFC to provide more detailed information about development impact at the project level. At a bare minimum, DFC should include the ex-ante development scores of its investments in its project database, update them as appropriate, and publish its ex-post results. In addition, DFC should aggregate and annually publish its development outcomes and private finance mobilization figures at the agency level to enable stakeholders to assess value for money.

8. Better define and strengthen the role of the Chief Development Officer. The BUILD Act created the role of Chief Development Officer (CDO), outlining several core responsibilities for the position. To insulate the CDO from any potential political pressure, the appointed individual reports directly to DFC’s Board. While well-intentioned, this arrangement carries the risk of isolating and marginalizing the CDO by placing the individual outside the management of the agency. A better alternative would have the CDO report both to the Board and to the CEO. The CDO’s role would be redefined as monitoring, evaluating, and maximizing overall development impact at the strategic agency level and assessing DFC’s performance in achieving the right balance across the agency's objectives. The head of DFC’s Office of Development Policy would remain responsible for ex-ante and ex-post measurement and reporting of impact at the transaction level and would play an enhanced role in embedding impact considerations in transaction development and approval.

9. Reduce burdensome reporting. Lawmakers should consider channeling some of World Bank President Ajay Banga’s recent energy for reducing directives that can delay projects by increasing the threshold of investments subject to congressional notification. There’s no question that Congress has an important oversight role to play, but the current requirement to submit a CN for any commitment over $10 million sets an extremely low bar that encumbers agency staff. Over the past four fiscal years, more than half of DFC transactions have cleared $10 million (averaging over 60 transactions annually).[4] If that hurdle had been set at $50 million, DFC would still have notified key committees about 17 percent of the agency’s investments (roughly 20 transactions annually). This higher threshold for reporting would still provide Congress with timely insight into DFC’s largest planned deals without overly taxing agency resources.

[1] EMDEs’ Current GDP, IMF World Economic Outlook, October 2023

[2] The European Energy Security and Diversification Act of 2019 was included in the FY2020 Further Consolidated Appropriations Act.

[3] DFC Active Projects as of 09.30.2023, FY2020-FY2023

[4] DFC Active Projects as of 09.30.2023, FY2020-FY2023

Disclaimer

CGD blog posts reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions.

Image credit for social media/web: W.Scott McGill / Adobe Stock