The International Monetary Fund (IMF) needs more subsidy resources to continue its concessional lending to low-income countries (LICs) at current levels. Following the example set by the United Kingdom, lenders to the IMF's Poverty Reduction and Growth Trust (PRGT) can build subsidy resources into their loan agreements. The relative cost is small and, in many countries, need not impact government budgets directly, as Special Drawing Rights sit on the central bank balance sheet. Here’s how.

How the PRGT works

The IMF uses its Poverty Reduction and Growth Trust to provide concessional loans to low-income countries. As we previously noted, demand for loans from the PRGT has been high since the COVID-19 pandemic. Given LICs’ high financing needs and the challenging global economic environment, demand is expected to remain high.

The PRGT borrows money from advanced economy countries at market rates and onlends that money to LICs at a below-market rate (now 0 percent). The loans made to LICs are repaid in 10 years, but principal repayments start after five and a half years, so that the average effective duration of the loan is 7.75 years.

When an advanced economy country loans funds to the PRGT, it gives up the interest it would have earned by keeping those funds on its balance sheet. In the case of recycled Special Drawing Rights (SDRs), the cost is the forgone interest on excess SDRs, or interest paid if the country’s SDR holdings are less than its allocation. In either case, the opportunity cost of the lending is the SDR interest rate, which is set to reflect global interest rates. During the pandemic, it fell to 0.05 percent, and it is now 3.85 percent.

The PRGT agrees to pay interest on the loan from the advanced country at the SDR interest rate to compensate the donor for its lost income. And since the PRGT charges the LIC that receives the loaned funds only zero percent, there is a gap to be filled. For most donors, the PRGT fills this gap using funds from the subsidy account.

How following the UK’s example could relieve pressure on the PRGT

When it lends to the PRGT, the UK largely forgoes the compensatory interest from the PRGT, absorbing almost all the subsidy to the LIC loan on its balance sheet. The loans from the United Kingdom receive an interest rate of just 0.05 percent, and thus draw only minimally on the subsidy account.

Other countries following the UK example would greatly relieve the pressure on the PRGT subsidy account and allow more PRGT lending. As noted in our earlier blog, lending from the PRGT can only occur if the IMF is certain that enough subsidy resources will be available to compensate the advanced economy country contributor. As interest rates have gone up of late and the PRGT lending rate has remained at zero, the gap that the subsidy account must fill has risen. So inevitably, every subsidy dollar can support less lending.

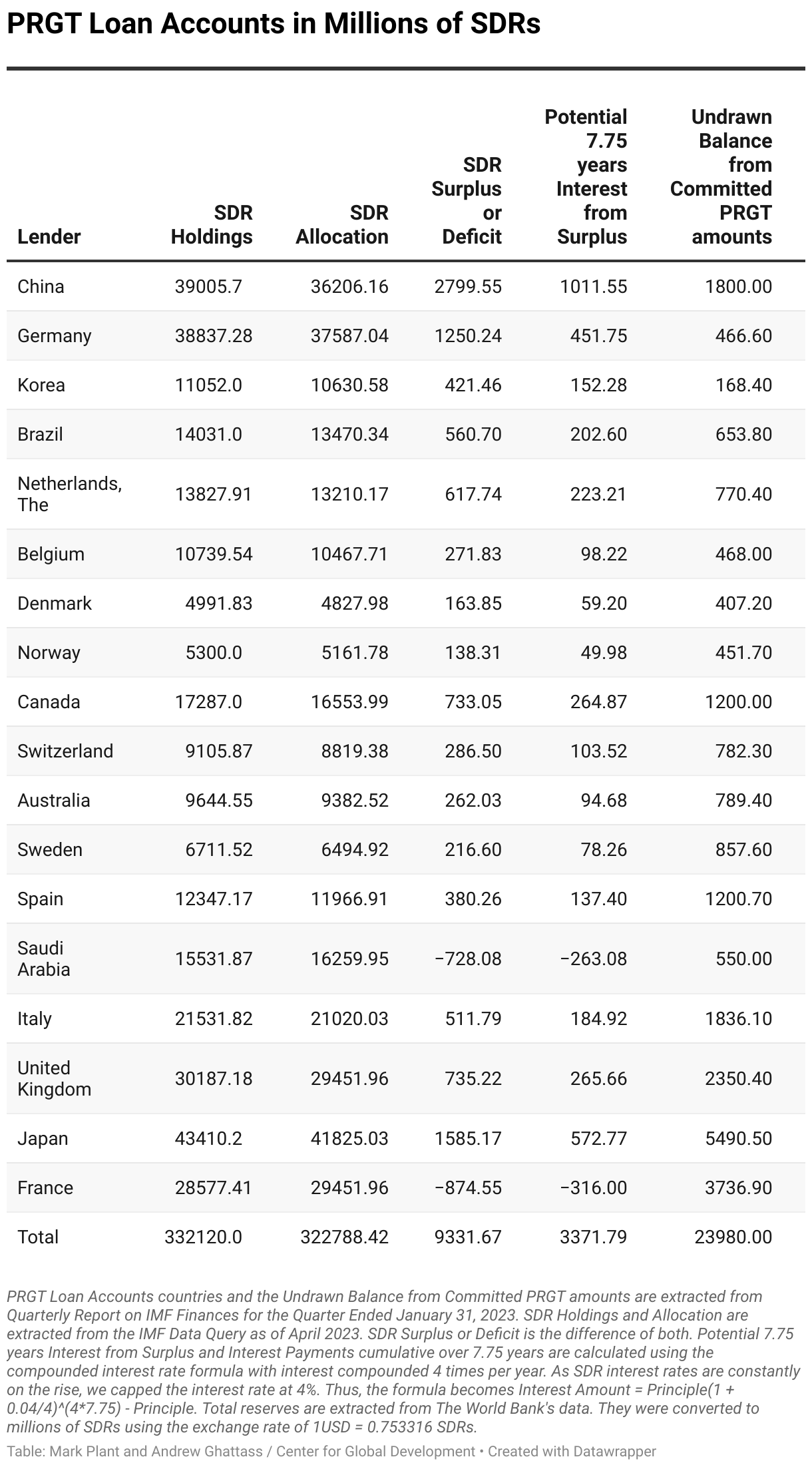

While following the UK example could seem costly in absolute terms, the costs are relatively small compared to the overall size of most countries’ reserves. To see this, we have to examine some numbers. Table 1 looks at the SDR positions of all the contributors to the PRGT.

The first two columns show the SDR holdings (how much they currently have) and SDR allocations (how many SDRs the IMF allocated to them). The third column is the difference—the surplus (or deficit) holdings. When a country has surplus SDRs, it earns interest at the SDR interest rate, and when it has a deficit, it pays interest at the same rate. In the fourth column of the table, we assume a relatively high SDR interest of 4 percent and calculate the cumulative 7.75 years of SDR interest earnings if the surplus stays the same. (Negative numbers indicate interest paid due to a deficit in holdings relative to allocation.) Thus, the first row of the table shows that China would receive slightly over SDR 1 billion in interest under current circumstances, while the last shows that France would pay just over SDR 0.3 billion in interest.

In the fifth column, we show the undrawn commitments to the PRGT. Each of these countries has committed to lend to the PRGT, and many have already done so, but only some of the pledges have been tapped for loans to LICs. Supposing the extreme case that IMF activated all these commitments today, the sixth column shows the interest payments that would need to be paid to the lending country to compensate for interest lost. For example, if tomorrow China lent the PRGT the SDR 1,800 million it has committed, the interest cost would be SDR 650 million over 7.75 years. The largest potential lender is Japan, whose interest cost would be almost SDR 2 billion for 7.75 years.

7.75 years’ worth of interest at the rate of four percent is a lot of money. But is it all that much when seen relative to the overall financial position of a country?

In most countries, SDRs belong to the central bank, so SDR recycling (or lending) to the PRGT would have an impact on the central bank reserves. Accumulated interest on SDRs would augment reserves, and any forgone interest would deplete those reserves.

Suppose another country follows the UK’s lead and lends to the PRGT but forgoes interest repayment. How much would reserves be affected? Only a little. The seventh column in our table shows total foreign reserves at the end of 2022, and the eighth column shows potential forgone interest as a percentage of total reserves.

The numbers are not significant. The UK is one of the most heavily impacted countries, and even it will only forego reserve accumulation amounting to 0.64 percent of current reserves. The impact in relative terms for China is negligible at a loss of 0.03 percent, a function of t vast foreign reserves accumulated over the last several decades. The cost to Germany would be SDR 168.6 million, a fraction of the SDR 1.4 billion (US$1.9 billion) Germany pledged to IDA, the World Bank’s concessional lending arm, for its most recent replenishment in 2021. And countries lending to the PRGT get their SDRs back when the loans are repaid ten years down the line, so their capital is never lost.

A few notes on our analysis. First, we've exaggerated the interest cost by assuming a 4 percent SDR interest rate. If global interest rates moderate, the costs will be less, as will the burden on central bank balance sheets. Second, some lending to the PRGT is by the government, not the central bank, which could have a budgetary impact. In some instances, the central bank will do the lending and require the government to cover any losses. The cumulative interest payments (column 6) might be significant for a government budget to swallow in one gulp (although over ten years, the pain would be lessened). Third, all the governments listed have already negotiated loan agreements with the IMF. Following the UK’s example may require renegotiation, which could require legislative or regulatory approval depending on the country.

But the essential point remains. Most countries that have committed to lending to the PRGT have surpluses of SDRs on which they are earning interest. Forgoing those interest payments for ten years will have a minor impact on the balance sheets of advanced economy countries. But doing so will enable much more lending from the PRGT and could have an enormous effect on LIC finances.

Disclaimer

CGD blog posts reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions.

Image credit for social media/web: Adobe Stock