Recommended

Blog Post

Imagine for a moment, that one of the roughly 31 million women in Ethiopia who are excluded from the financial system wants to get a bank account. What would she have to do? In many cases, she would have to start by getting an ID.

We know that ID is a foundational enabler for development, and the Sustainable Development Goals recognize this as well, establishing legal identity as SDG Goal 16.9. An ID enables the woman to open a bank account, which she can use to receive and make transfers, save, and transact in the formal economy. Likewise, in each of about 150 countries that require SIM registration, an ID allows her to obtain a mobile phone and SIM card to transact remotely. That means fewer trips to the bank branch and an alternative to cash. But this only scratches the surface of the development possibilities enabled by having an ID, a bank account, and a mobile phone.

As the United Nations General Assembly meets this week, global leaders will be taking stock of their countries’ progress towards the SDGs and mapping out where they still have to go. Our research has shown that, together, financial accounts, ID, and mobile phones can facilitate a wide variety of cross-cutting programs to meet the SDGs, which can be cost-effective at scale.

So, as policymakers strategize on their approaches to meeting the SDGs by 2030, we want to take a closer look at how governments can use these three tools to do just that. While many of these applications are still ”frontier” and not yet fully mature, the signs are positive that they are having an impact. To understand this better, we cluster together SDG targets and briefly describe how governments are using a combination of ID, bank accounts, and/or mobile phones to improve their performance. These are not necessarily comprehensive solutions to all SDGs in each cluster, nor do they represent the limits of these platforms, but we connect them here to illustrate how they can be a jumping-off point for policymakers.

SDG Cluster 1: Access to ID, Financial Inclusion, and Mobile Phones

Goal 8.10 Strengthen the capacity of domestic financial institutions to expand access to financial services for all

Goal 16.9 Provide legal identity for all, including birth registration

Goal 17.8 Enhance the use of technology, in particular ICT; Proportion of individuals who: own a mobile telephone; are covered by a mobile network; use the Internet

India’s Aadhaar program has enrolled over a billion people into its biometric identification program and is coming very close to universal coverage among adults. Aadhaar enables people to verify their identity using biometric data queried off a central database rather relying on paper records. Pakistan and Peru, among other countries, have implemented comprehensive ID systems. This enables mobile network carriers and financial institutions to comply with Know-Your-Customer requirements more easily and cheaply, as in India where both mobile inclusion and financial inclusion have made huge gains since the rollout of Aadhaar.

SDG Cluster 2: Efficient Pricing and Sustainability with Equity

Goal 6.4 Increase water-use efficiency

Goal 11.6 Reduce the adverse environmental impact of cities, including air quality; Mortality rate attributed to household and ambient air pollution

Goal 12.c Rationalize inefficient fossil-fuel subsidies, phase out to reflect environmental impact, and minimize the possible adverse impacts on the poor

Goal 12.2 Achieve the sustainable management and efficient use of natural resources

Goal 15.2 Sustainable management of forests, halt deforestation, restore degraded forests

Most economists agree that a carbon tax is the optimal solution for fighting climate change. This will inevitably impose a higher burden on poor consumers unless offset through compensatory transfers. The trio of ID, bank account, and mobile phone can help governments to better implement targeted subsidies to compensate these affected groups, to ensure poor consumers don’t bear most of the burden for stopping climate change.

In 2010, Iran implemented an oil-for-cash program in 2010 which leveraged the country’s robust identification system to eliminate economy-wide price controls on oil and replace them with a uniform household transfer delivered directly to bank accounts. Likewise, India’s cooking gas subsidy program was reformed using the Aadhaar platform to deliver subsidies directly to beneficiaries’ bank accounts, allowing the government to remove market price distortions while simultaneously enjoying cost savings by eliminating duplicates and ghost beneficiaries and reducing leakage and corruption. A carbon tax subsidy for poor consumers could work much the same way, and just as successfully.

SDG Cluster 3: Poverty and Social Protection

Goal 1.3 Implement social protection systems for all

Goal 2.1 End hunger and ensure access to safe, nutritious and sufficient food

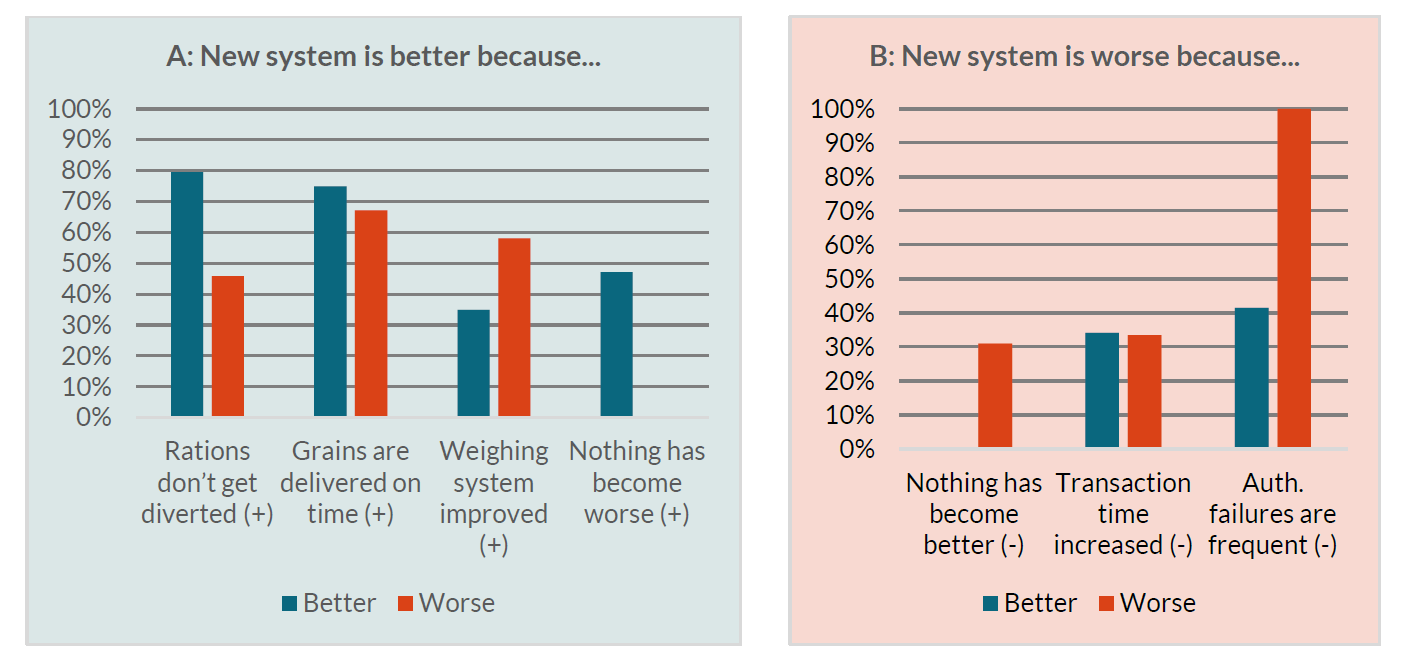

Our recent work in the Indian states of Rajasthan and Andhra Pradesh suggest that social protection could benefit significantly from the integration of IDs, bank accounts, and mobile phones, because they allow governments to accurately deliver benefits to vulnerable groups. In Rajasthan—a relatively middle-of-the-pack performer in terms of state capacity—our surveys found that beneficiaries were more likely to prefer digital biometric verification to receive food rations and social pensions because it increased their agency and improved the regularity of deposits. In the state of Andhra Pradesh, which has more advanced governance capacity, even larger majorities preferred the digital systems: 70 percent for food ration beneficiaries and 84 percent for social pension recipients.

SDG Cluster 4: Frictionless Payments

Goal 1.4 ensure that all men and women, in particular the poor and the vulnerable, have equal rights to economic resources, as well as access to basic services, appropriate new technology and financial services, including microfinance

Goal 3.8 Achieve universal health coverage, including financial risk protection

Goal 10.c Reduce remittance costs to less than 3 per cent

Goal 17.1 Strengthen domestic resource mobilization

Kenya’s move towards government digitization has improved domestic resource mobilization; it has been able to expand the tax base (including on mobile money transfers) and close off opportunities for leakages and fraud. The prevalence of IDs and mobile phones has lifted the country’s financial inclusion rate from 42.3 percent in 2011 to an impressive 81.6 percent in 2017, driven in large part by mobile money adoption.

SDG Cluster 5: Effective and Accountable Governance

Goal 16.5 Reduce corruption and bribery in all their forms

Goal 16.6 Develop effective, accountable and transparent institutions at all levels

As seen in Kenya and Tanzania, digitizing person-to-government payment systems can reduce petty corruption and opportunities to exact rents. Andhra Pradesh has been at the frontier of innovation with a feedback system that holds its bureaucracy accountable to performance outcomes. Andhra Pradesh’s real-time governance system proactively solicits feedback from all beneficiaries after they interact with a service using robo-calls, transferring dissatisfied clients to a call center and maintaining a 24-hour grievance redressal timeline. User satisfaction scores are used to compute a “Happiness Index” for each district, which drive goal setting and accountable governance.

SDG Cluster 6: Empowering Women

Goal 5.a Give women equal rights to economic resources, as well as access to ownership and control over land and other forms of property, financial services, inheritance and natural resources;

Goal 5.b Enhance the use of enabling technology, in particular ICT; to promote the empowerment of women

Bangladesh offers an example of how a government can take advantage of ID and mobile phones to shift an existing program onto a digital infrastructure. Bangladesh linked the payments for the Primary Education Stipend Program, which provides government stipends to poor families to encourage educational participation, to mother’s mobile bank accounts. We carried out a small survey of households who receive the stipend as well as school headmasters who implement it and found that 79 percent of mothers and 80 percent of headmasters preferred the new, digital system. The flexibility of the direct deposit into mobile accounts freed up mothers from having to visit schools to receive the stipends while offering many their first opportunity to hold a mobile money account. Headmasters were relieved of the need to administer cash payments and less liable to be accused—rightly or wrongly—of corruption.

This is not an exhaustive list of potential interventions or applications, but a mere taste of how governments can use the trio of mobile phones, ID, and bank accounts to meet the Sustainable Development Goals. Of course, each possibility depends on institutional and infrastructural factors which can affect implementation. Likewise, without purposeful measures to ensure a program serves marginalized people, it can instead amplify existing biases and inequalities. But the potential to affect citizens’ lives in good or bad ways is also our point: technology is power, and power can be used by governments to serve their people.

Disclaimer

CGD blog posts reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions.

Image credit for social media/web: Photo by Mpande / Wikimedia Commons