Often overshadowed by the regional powerhouses that border it, Paraguay’s recent sovereign bond issuance of $530 million was five times oversubscribed, revealing that the landlocked country of 7.5 million people warrants more attention. With presidential and legislative elections approaching next month, the incoming government will surely hope to continue building upon the country’s recent economic growth, averaging 4.8 percent over the last decade. This growth has helped the country make massive poverty reductions in one of the lowest income per capita countries in Latin America—in 2016, Paraguay’s poverty rate was 26 percent, down from 57.7 percent in 2002.

This success has been largely thanks to sound macroeconomic management that has helped the country weather both political and economic uncertainty in two of Paraguay’s major trade partners, Brazil and Argentina. However, as protectionist forces gain strength in the United States, interest rate hikes by the Fed are certain, and renewed market volatility raises concerns, structural shortcomings threaten to diminish the country’s capacity to withstand external shocks. The persistent vulnerability to such shocks demands attention be paid to how structural variables undermine Paraguay’s resilience and reduce the effectiveness of its macroeconomic strengths.

Indicator of economic resilience to external shocks

The importance of structural variables is revealed in my latest CGD working paper, which constructs an indicator of economic resilience consisting of two dimensions: (i) the economy’s capacity to withstand the impact of the shock, and (ii) the authorities’ capacity to rapidly implement policies to counteract the effects of the shock on economic and financial stability. Each dimension consists of both macro and structural variables. While macro variables can fluctuate rapidly in the short run, structural variables take more time to change. Inadequate performance of the latter can limit the effectiveness of the former, downgrading resilience against shocks.

The figures below illustrate the dimensions of resilience with macro variables in black and structural variables marked in red.

Figure 1. First dimension of resilience: the capacity to withstand the impact of the shock

In the event of an external shock, non-domestic sources of finance can become scarce and costly. Thus, the first dimension of Paraguay’s resilience depends on the strength of its external position and the availability of domestic sources of finance. The former is a testament to the country’s prudent macroeconomic management. In 2017, Paraguay boasted a current account surplus (as a percentage of GDP) and a total debt ratio of only 25 percent of GDP. Strong performances in these macro variables supported demand for Paraguay’s recent bond issuance, reflecting their importance as a safeguard against external shocks.

At the same time, Paraguay’s structural variables moderate such strengths and undermine its capacity to withstand shocks. First, trade shocks represent an important risk to Paraguay where soy and derivatives, cereal and beef account for about 75 percent of exports. In the event of a sharp decline in prices for these products, the lack of export diversity can expose Paraguay’s external position to current account balance deterioration and a weaker fiscal stance. Second, the national savings rate and indicator of financial depth are woefully low. Paraguay’s savings ratio is less than 20 percent. This helps explain Paraguay’s low level of financial depth that is hampered by a stubbornly low pension funds ratio. Together, these deficiencies signal a lack of domestic sources of finance needed to counteract a sudden scarcity and/or higher costs of external sources of finance.

Figure 2. Second dimension of resilience: the capacity of authorities to rapidly implement policies to counter the effects of the external shock

With respect to the second dimension of economic resilience, the story is quite similar. Efforts to improve the country’s macroeconomic stance since 2003 have paid off and will continue to do so if a new adverse external shock hits the economy. During the global financial crisis, the authorities had the fiscal and monetary space to implement countercyclical policies, minimizing the overall effect of the shock. An analysis of Paraguay’s macro variables presented in my paper reveals that their relative strength has persisted, and in some cases, such as the behavior of inflation under an inflation targeting scheme, has even improved.

Again, the strength of these macro variables needs to be qualified by Paraguay’s structural deficiencies! Tax collection in the country is one of the lowest in Latin America. Despite a low fiscal deficit and debt, weak tax revenues can potentially undermine Paraguay’s ability to fund existing investment projects in the event of a shock that reduces or reverses external sources of funding. Additionally, Paraguay’s rate of financial dollarization, measured as financial institutions’ holding of assets and liabilities denominated in foreign currency, is nearly at 50 percent. The latter is contained because a significant part of borrowings in dollars corresponds to the agribusiness industry, whose revenues are denominated in dollars and, therefore, have a natural hedge. Notwithstanding, a high degree of dollarization remains a risk to financial sector stability and a constraint on the efficacy of the central bank to respond countercyclically to an adverse external shock.

Ranking Paraguay: the significance of structural variables in Paraguay’s performance relative to other emerging markets

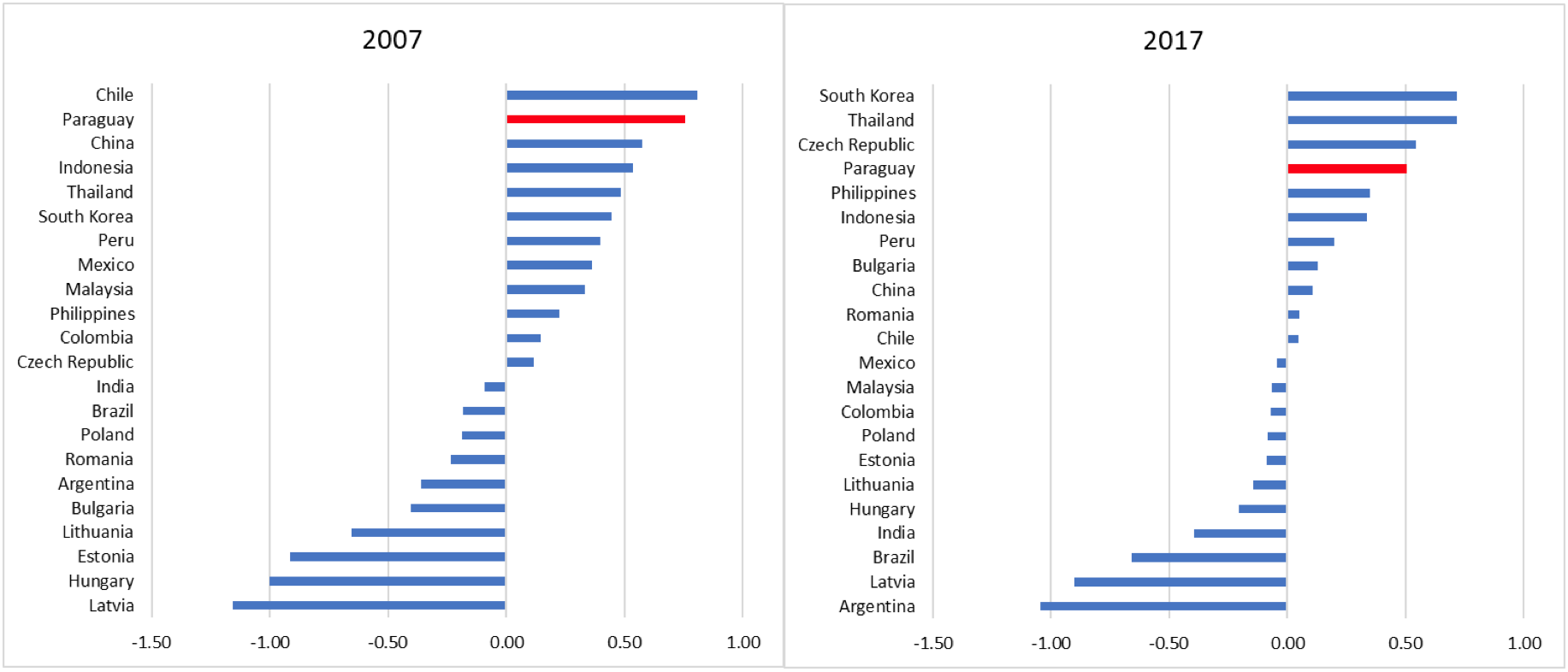

To evaluate Paraguay’s economic resilience and highlight the importance of structural variables, I put together two valuable exercises. First, similar to the exercise in my 2015 paper and using a similar methodology, I consider the macro variables discussed in this blog post to create a macroeconomic resilience indicator that is defined as the simple average of the seven variables in consideration. The two graphs below compare how this ranking has changed in the last decade, presenting the indicator’s values in 2007, pre-global financial crisis, and 2017. Countries are organized according to the value of the indicator. The larger the value, the greater the country’s macroeconomic resilience relative to the countries in the sample.

Figure 3. How the macroeconomic resilience indicator value affects country ranking, 2007 and 2017

Paraguay only moves from second to fourth place in the ranking between 2007 and 2017, confirming the macroeconomic strengths discussed in this blog post. Yet, a second exercise that accounts for all variables considered in this blog post (macro and structural) paints a different picture.

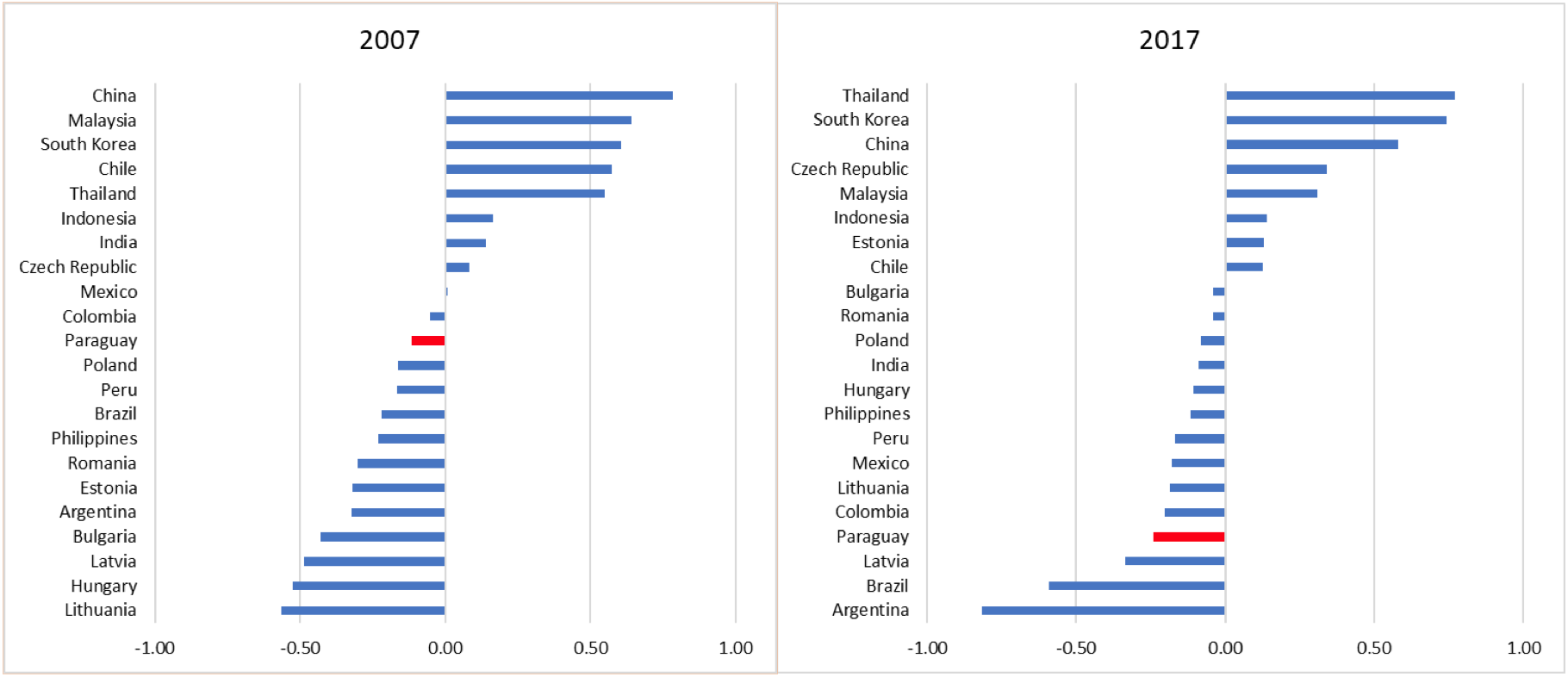

Here we employ an indicator of economic resilience to external shocks that accounts for all the variables considered in this blog post (macro and structural).[i]

Figure 4. How the economic resilience to external shocks indicator value affects ranking, 2007 and 2017 (all variables, macro and structural)

In this exercise, the effect of structural variables is clear. Paraguay’s position is not only lower than in the first exercise, but its position deteriorates considerably from position 11 to 19 out of the 22-country sample.[ii]

In Paraguay, the winners of next month’s elections will face the challenge of building upon Paraguay’s pragmatic macroeconomic management by bolstering its economic resilience through structural reforms. Considering that a more uncertain external environment looks increasingly likely, it truly is an opportunity that Paraguay can’t afford to waste.

[i] Four sub-indicators are considered represented in the two dimensions of resilience (external position, availability of external financing, fiscal position and monetary position). Each sub-category is formed by the corresponding variables discussed previously. These sub-categories are obtained by calculating the simple average of the standardized values of the variables that they’re comprised of. Finally, the indicator of economic resilience to external shocks is the simple average of the four sub-indicators.

[ii] This exercise considers tax revenue—an index without this variable is presented in the working paper where Paraguay falls from position 9 to 12 in the ranking.

Disclaimer

CGD blog posts reflect the views of the authors, drawing on prior research and experience in their areas of expertise. CGD is a nonpartisan, independent organization and does not take institutional positions.

{kind=link}

{kind=link}